View all blogs

Recent trends in liability insurance (2025)

Market insights

By

Insuraviews

September 9, 2025

.png)

YTD, Other Liability is running “two‑speed.” On a premium‑weighted basis across your filings, the line is up ~7.44%on an implied affected base of ~$7.77B,producing ~$578M of premium change. Most exposure sits in modest adjustments, but a narrow band of umbrella‑heavy moves accounts for an outsized share of dollars. In our dataset, State Farm + Allstate (umbrella‑heavy)generate ~43% of all change dollars off just ~7% of the implied base—evidence that Personal Umbrella is doing the heavy lifting for overall liability rate adequacy while Commercial GL stays comparatively tempered.

Geography concentrates the dollars while rate heat varies by region. New York, California, and Texas together drive ~36% of total change dollars. By effective rate, the Midwest(~14.5%) is the hottest region, ahead of the South(~9.0%), East (~7.0%),and West (~4.7%). That mix echoes an umbrella‑led story in several Midwestern states, while the West’s larger bases often move on lower single‑digit prints.

.png)

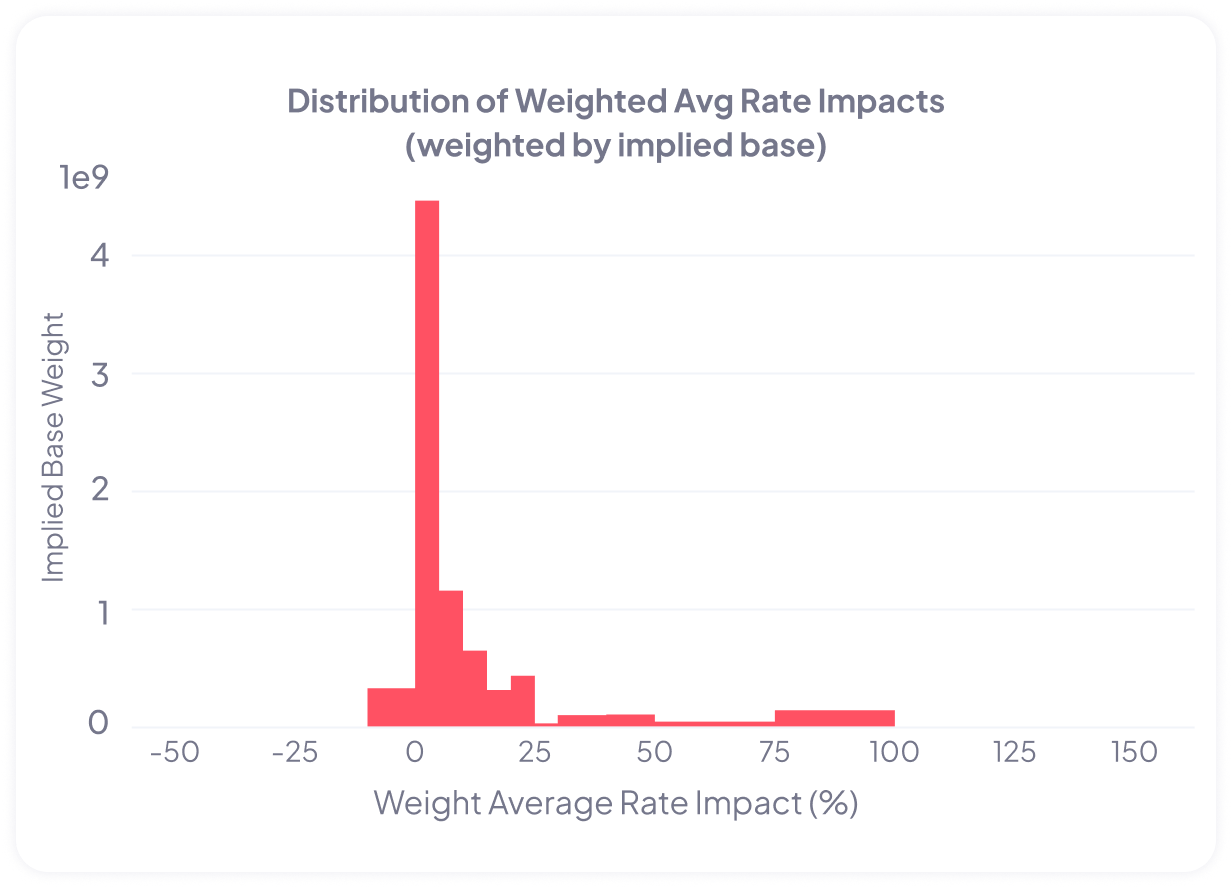

Distribution matters—most base is moderate, a small slice is extreme. Roughly 72% of the implied base sits in the 0.1–9.9% impact tier, 18% in 10–24.9%,and only ~2.5% in ≥50% changes. Those extreme cells are few in number but highly visible and concentrated in umbrella filings; they shape market perception even though most insureds are seeing single‑ or low‑double‑digit GL moves.

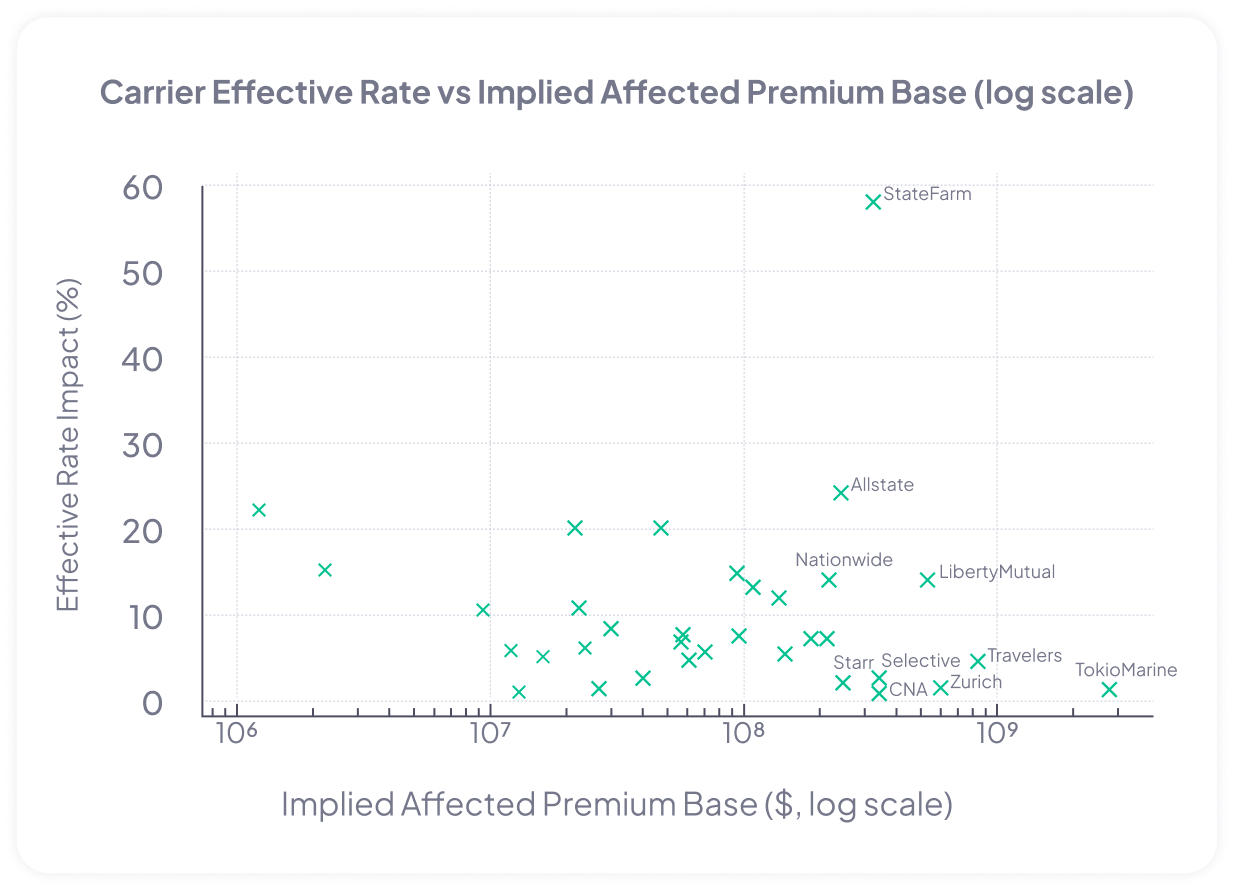

Carrier dynamics show an umbrella spike and GL restraint. State Farm contributes ~32.5% of all change dollars with an effective ~58% on ~$325M of implied base. Allstate is next among umbrella carriers (effective ~24%),while GL incumbents with very large books appear measured: Tokio Marine (implied base ~$2.63B) moved only ~1%, and Travelers printed ~4.7% on ~$819M—a classic share‑defense posture. A notable counter‑trend pocket: Louisiana shows a –6.7% net effect (led by Travelers), one of the few state‑level deflations in the dataset.

State outliers and cell extremes validate the umbrella thesis. Among states with meaningful base (≥$25M), premium‑weighted effective rates peak in Washington (~47%), Michigan (~35%), Maryland (~34%), and Kentucky (~27%); California still prints a hefty ~19.5% on a very large base. At the cell level (≥$5M implied base), State Farm posts ≥70%in WA, WI, MI, CA, UT, and Allstate shows ~75% in Alabama, matching the directional guidance in their umbrella filings. Those proposals include ~100%‑scale changes in WA/MO and 75%+in MI/WI, with ~50% in TX, reinforcing the umbrella-centric rate picture.

State Farm’s execution playbook blends big asks with guardrails. The filings pair large PLUP increases with per‑insured caps (e.g., 25% in GA/NJ), selective non‑prior‑approval routes to accelerate timing, and even de‑emphasis of credit scoring/claims history in Georgia—a notable segmentation shift. The record shows rigorous objection handling (e.g., Washington at ~99.7% proposed) and transparent actuarial justification, which helps explain how extreme umbrella moves are being implemented without wholesale customer flight.

Allstate’s umbrella strategy emphasizes scalable mechanics and analytics. Across multiple states, Allstate leans on Rate Adjustment Factors (RAFs) to lift premiums without re‑wiring territorial/class relativities—useful for speed and regulatory clarity. Outliers include ~75% in Alabama and 35%+ where loss ratios approach ~90% (e.g., CA/MI), alongside fee optimization (e.g., Michigan)and explicit use of Fama–French factors (e.g., North Carolina) in actuarial work. Several filings affect very large policyholder cohorts (e.g., Texas), underlining the scale of the umbrella recalibration.

Liberty Mutual’s GL filings show wide dispersion, product refinement, and ISO anchoring. Big increases—~74.8% CT, ~60.8% NC, ~52.6/44.9% GA, ~49.7% CA—coexist with –1.3% in Massachusetts, highlighting localized loss cost pressure and competitive dynamics. Liberty frequently adopts/adjusts ISO loss costs, adds new class codes (e.g., snow plowing, technology), and addresses punitive damages (NY)and Sexual Misconduct terms(IN), signaling a mix of technical pricing and form hygiene rather than blunt across‑the‑board hikes.

Berkshire’s heterogeneity, Progressive’s compliance focus. Berkshire shows sharp Liquor Liability divergence (GA+43% vs. ID –3%,ME ~flat), modest EPL rate trims paired with optional Fiduciary and enhancements for workplace violence/biometric privacy—a nuanced, segment‑by‑segment craft. Progressive focuses on Nevada GL forms to align cancellation/adverse‑action notices with FCRA, underscoring an industry trend toward regulatory UX and communications clarity.

Moderate GL, targeted innovation, and evolving exclusions. The general2025 scan captures Travelers OMNI II GL increases of roughly ~10% (NY)and ~3.3% (TX), Starr at ~5%in NY, and Selective in the 3–6% range—consistent with the measured GL posture we observe in the data. Product tweaks like Travelers’ “Choice of Counsel” endorsement and medical stop‑loss options expand flexibility, while PFAS and Abuse/Molestation exclusions continue to propagate. Some sector‑specific GL pushes (e.g., tech classes at Zurich) encounter approval friction, a reminder that regulatory alignment remains a gating factor.

© 2026 Insuraviews. All rights reserved.