View all blogs

Accelerate approval: resolving complex LAE & combined ratio objections with Insuraviews

Market insights

By

Insuraviews

March 5, 2026

Safeco’s Maryland Homeowners rate filing LBPM-133578830 is a textbook example of a high-stakes rate action caught in regulatory friction. The carrier is seeking a significant premium increase with an initial indicated need of 23.9%, though the proposed impact is being communicated as a 12% rate impact. This filing directly affects 20,105 policyholders and locks up a substantial $3.9 million in additional written premium.

Regulatory hold-ups are more than an administrative delay. For a carrier, every day the proposed rate is not in effect represents a direct loss of critically needed premium. This lag jeopardizes solvency and underwriting profitability. The challenge intensifies when Department of Insurance (DOI) objections hinge on complex, actuarial justification points.

The core problem here is not the rate itself, but the justification for key components. Specifically, the filing received complex objections regarding its historical Combined Ratio Information and the rationale for the Loss Adjustment Expense (LAE) Factor. These objections are universally high-friction points.

Regulators are acutely focused on two metrics: a carrier's long-term financial health and the justification for every cost component passed to the consumer. The objections in this filing strike at the heart of both.

The Combined Ratio is the most immediate indicator of underwriting performance. The filing context reveals a challenging environment, with the company’s combined ratio escalating sharply to 121.6% in 2022 and sitting at 106.8% in 2021. Regulators demand a clear, comprehensive, and multi-year history to validate the need for the rate increase. Simply stating the figures is insufficient; the trend must be justified with credible data.

The Loss Adjustment Expense (LAE) Factor objection is a matter of granular precision. The DOI pointed out a discrepancy between two exhibits in the justification documents. While the original filing suggested a 12.1% LAE-to-Loss ratio, the corrected justification confirms the selection of 12.8%. This 0.7 percentage point difference may appear minor, but it relates directly to the calculation of the permissible loss and expense ratio—a key regulatory benchmark set at 69.7%. Justifying this final selection requires a robust, competitive, and state-specific analysis to prove it is not excessive.

The root of most regulatory friction is a failure to provide contextual expertise. A carrier’s internal actuarial justification, while sound for internal use, often lacks the necessary competitive, public-facing data to satisfy a DOI reviewer. The reviewer needs to know, definitively, that the carrier's selection is not an outlier and is based on sound, market-verified principles.

The traditional response mechanism is time-consuming and prone to compounding error. Once an objection is received, a carrier's team must:

This analog, manual process is precisely where the innovative solution must reside. Competitor solutions may offer raw market data, but they fail to deliver the cited, actionable, and reviewer-ready justification that resolves the specific objection instantly.

Insuraviews has developed DOI Reviewer Support to bypass this high-friction point with true industry expertise. We don't just provide data; we provide the approved competitive precedent required to immediately satisfy the objection.

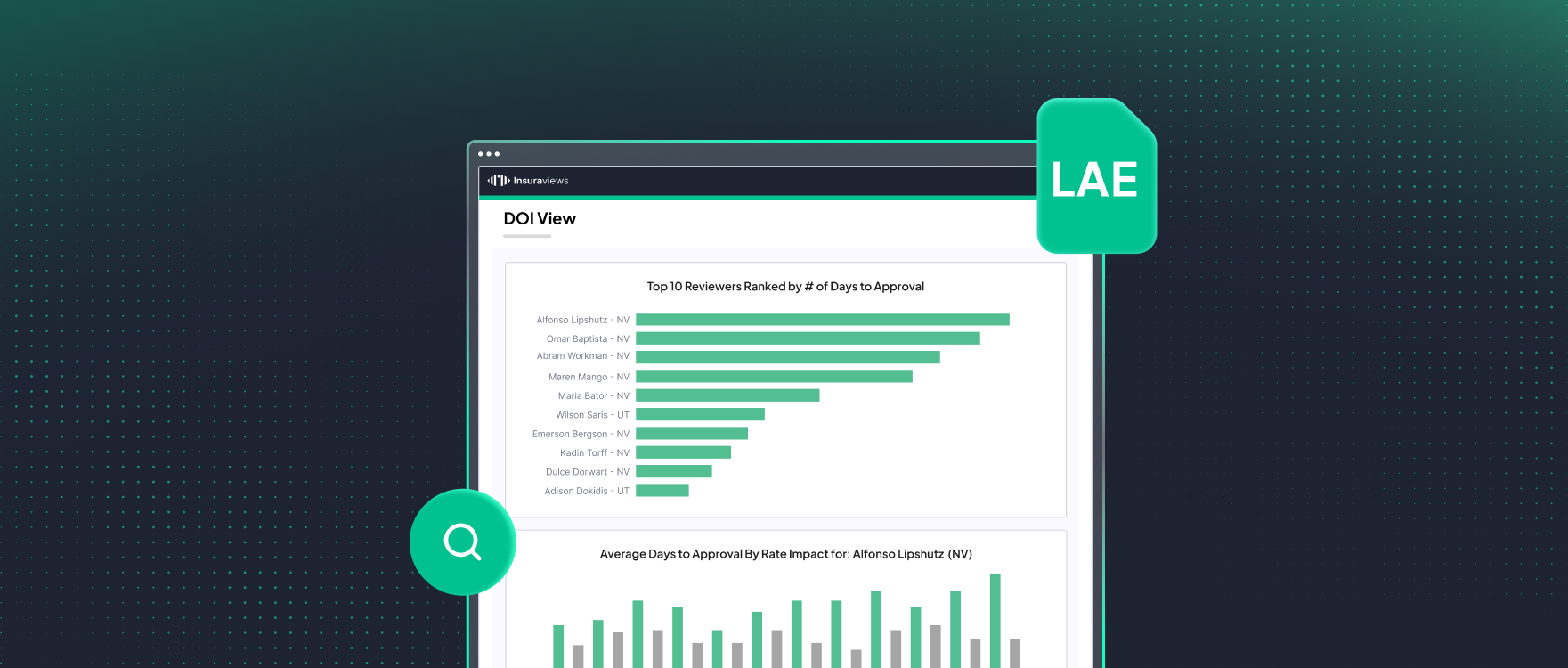

The feature works by cross-indexing the core metrics of your filing—such as the selected LAE-to-Loss ratio of 12.8% and the history of Combined Ratios—against our massive, proprietary database of approved competitive filings. When a specific objection, like the LAE discrepancy, is raised, our platform instantly surfaces:

This innovative, machine-speed resolution turns a multi-day research effort into an instantaneous, pre-approved response. It directly addresses the "Combined Ratio Information Objection" by providing a comprehensive, market-driven narrative that demonstrates a genuine need for the rate.

Regulatory efficiency is the ultimate competitive advantage in the insurance market. By leveraging DOI Reviewer Support, carriers can transform a complex, stalled filing into a swift approval. The ability to instantly resolve specific, technical objections—like the one surrounding the LAE Factor in the Safeco filing—means securing the additional $3.9 million in written premium weeks or even months sooner.

Our approach is not about tricking the system; it’s about providing superior, authoritative justification that meets the reviewer’s need for clarity, consistency, and competitive context. We protect your premium and deliver the highest level of regulatory confidence.

Don't let complex LAE and combined ratio objections delay your premium capture. See how DOI Reviewer Support can accelerate your next rate filing and protect your bottom line.

Visit insuraviews.com to request a demo of our DOI Reviewer Support.

© 2026 Insuraviews. All rights reserved.