View all blogs

Insuring the Backbone of America: A 2025 Review of the BOP Market

Market insights

By

Insuraviews

January 16, 2026

As we step into 2026, it's a good time to reflect on 2025 for the Business Owners Policy (BOP) market in the U.S. A BOP bundles key coverages for many small and medium-sized businesses. It often includes property, general liability, and business interruption coverage. In 2025, the market showed more stability than prior years. Rate movement cooled, and competition increased for well-managed accounts. Social inflation, catastrophe losses, and cyber risk continued to drive caution. Many carriers responded with targeted exclusions and endorsements. In this article, we'll break down the major trends, spotlight key updates, and examine strategies from industry players like Liberty Mutual and Hanover.

The U.S. commercial insurance market, including BOP, began to soften in Q4 2025 as premium growth slowed and capacity expanded across many lines. Social inflation remained a key pressure point. Higher jury awards and litigation costs drove much of that pressure. Uncertainty also persisted around catastrophe losses and claims severity trends.

For BOP, rate outcomes varied by coverage type. Non-catastrophe property rates were mostly stable or slightly higher. Liability lines faced continued upward pressure from nuclear verdicts and escalating claims.

Insurers increasingly differentiated risks based on documentation and loss prevention. Accounts with active safety programs, building maintenance, and risk controls saw more favorable outcomes. Overall, the U.S. property and casualty market projected stability despite broader volatility, with opportunities for flat or modest renewals for well-documented risks.

One of the most notable developments in 2025 was the Insurance Services Office (ISO) rolling out major BOP revisions. These changes became effective on July 1.

Key changes included broadened definitions, such as expanding mobile equipment to cover ATVs without focusing on vehicle registration, and extending coverage radii to 1,000 feet.

New exclusions addressed ransomware and electronic smoking devices. Eligibility classifications were revised for industries like auto services, contractors, and restaurants.

ISO also introduced 59 new endorsements. These addressed exposures related to drones, cannabis operations, and automatic additional insureds. Together, these updates reflect efforts to address emerging risks while preserving flexibility.

Rate fluctuations painted a mixed picture, but overall, rates increased for BOP in the U.S. The November 2025 Ivans Index showed year-over-year increases across most commercial lines. BOP premiums rose about 7.5%, commercial property increased around 8.1%, and umbrella rose roughly 9.2%. These increases were driven by claims inflation and higher loss costs. Workers’ compensation declined by 1.5%.

Market conditions showed upward trends, though growth slowed in some quarters. In Q2, BOP rates increased 2.6%, reflecting continued pressure from inflation and loss costs. In Q3, BOP increased 7.5%, slightly below Q2's 7.9%. This suggested moderation in the rate of growth, while remaining positive overall.

Cyber premiums dropped by up to 20% for firms with strong security controls. Property costs increased due to severe weather trends. Average monthly commercial building premiums are projected to reach $4,890 by 2030. In casualty lines, general liability increased up to 2.7%, excess liability rose 5.5%, and auto increased 7.4% due to repair costs and tariffs.

Cyber risks took center stage for BOP in 2025. ISO introduced new endorsements for cyber liabilities.

These updates included mandatory and optional exclusions for data privacy violations and cyber incidents. Coverage for electronic data and cyber-related damages remained limited. ISO also revised language to include biometric data. One endorsement was withdrawn and later replaced.

These changes aligned with broader market trends. Insurers responded to increased cyber activity and growing use of AI-enabled attacks. Some carriers also explored parametric solutions to address gaps in traditional cyber coverage.

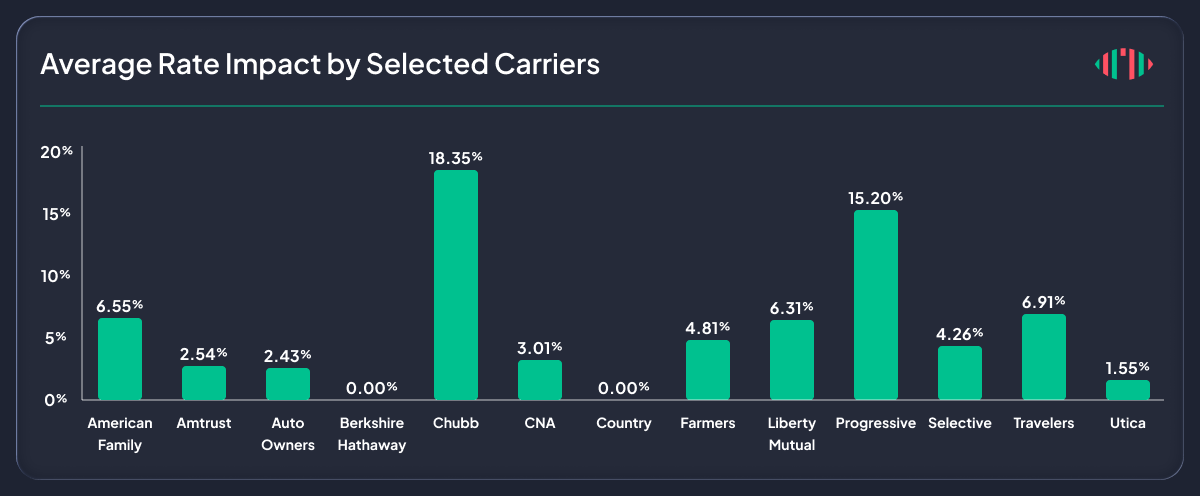

In 2025, major insurers like Liberty Mutual and The Hanover Insurance Group (including affiliate NOVA Casualty Company) chose selective non-adoption of ISO updates. These carriers prioritized state compliance, risk management, and competitive positioning over full implementation.

Liberty Mutual pursued widespread non-adoption of certain ISO forms and rules. Many of these changes carried zero rate impact. At the same time, Liberty implemented significant rate increases in several states. These included Kansas at 25.5%, Connecticut at 24.5%, New York at 25%, Wisconsin at 20.4%, Texas at 17.4%, New Jersey at 15.3%, Nebraska at 22.4%, South Dakota at 28.4%, and North Dakota at 31.9%.

Their filings emphasized exclusions for assault or battery, silica risks, violent acts, employment practices, and fraud-related cancellations. These filings were supported by detailed actuarial data under regulatory scrutiny in states like Maryland and Indiana. Emerging risks were also addressed through coverage extensions, including security breach claim reporting in Connecticut.

Similarly, Hanover introduced endorsements excluding war and cyber war losses. These endorsements defined terms clearly and applied automationally with cyber coverage. No premium charges were applied. Many of these endorsements were later withdrawn following internal review or limited insured impact. Regulatory responses varied by state. New York rejected some filings for non-standard definitions. Texas rejected others under exempt line rules.

NOVA also filed for non-adoption or delayed adoption of ISO designations. These filings occurred across states, including Pennsylvania, Nebraska, North Dakota, Georgia, and Connecticut. NOVA cited system limitations and class plan differences. Approved filings maintained no rate impact. NOVA's cyber war exclusions became effective December 1, 2025. These exclusions included clear definitions and contained no premium effect.

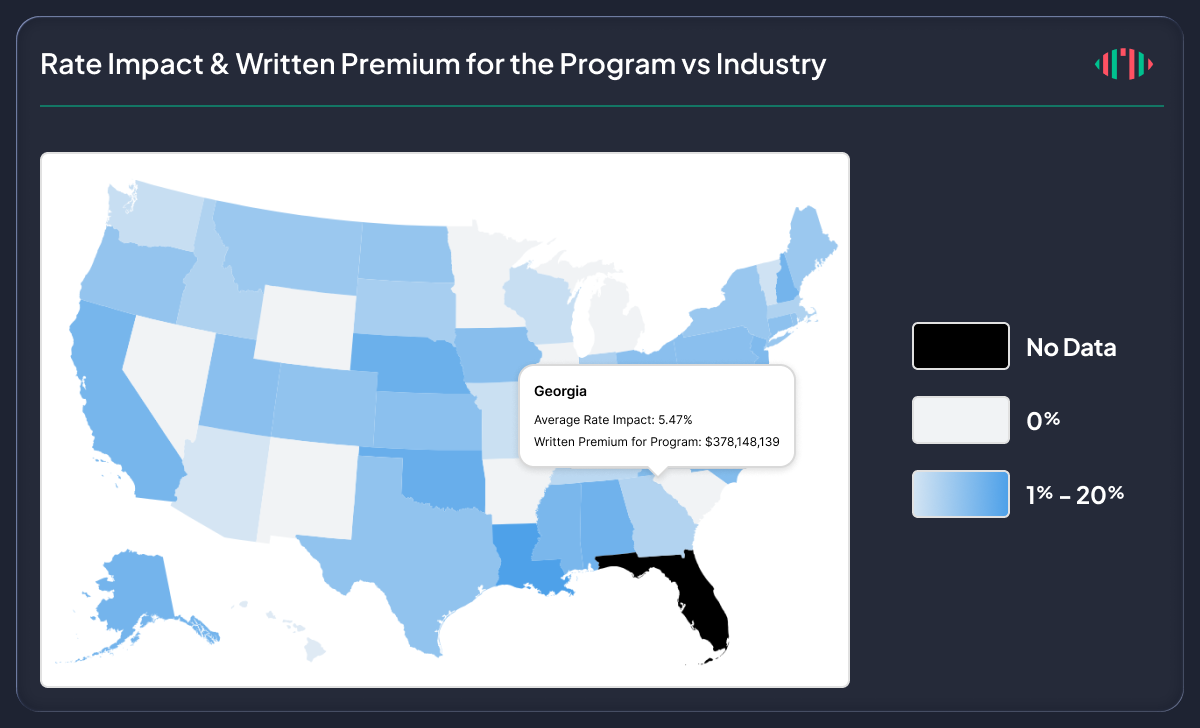

Georgia emerged as one of the most active states for BOP filings in 2025. Carriers, including Alfa, Central Mutual, Cincinnati, Encova, Federated, Liberty Mutual, and Progressive, drove rate revisions and product changes. These filings aimed to address underwriting results and loss experiences amid ongoing tort reform.

Key developments included substantial rate hikes from Liberty Mutual. Several Liberty Mutual BOP filings were withdrawn in early 2025 and later refiled in the second half of the year. Approved rate increases included State Automobile at 15.1%, Ohio Security at 7.9%, General Insurance at 17.5%, State Auto Property at 14.9%, Ohio Casualty at 8.3%, West American at 8.3%, West American at 8.3% and American Fire at 8.1%. Alfa and Progressive reduced requested increases following regulatory objections.

Central Mutual and Federated maintained neutral impacts. These carriers focused on rule and form updates. Federated and Encova adopted more granular ISO loss costs and peril differentiations.

Endorsements addressed emerging risks like assault and battery, cannabis, viruses, bacteria, and cyber liability. Strong regulatory coordination was reflected in multiple closed and acknowledged filings. Innovations included Liberty's tailored pricing for high-premium risks. These efforts balanced rate increases with regulatory feedback to refine coverages and competitiveness.

Georgia's April 2025 tort reform package by Governor Brian Kemp also influenced rate filing activity. The legislation limited damages, "anchoring" limits, and revised dismissal procedures. It also removed the collateral source rule. These changes may reduce social inflation and improve rate predictability. House Bill 902 added transparency requirements for rate increase postings beginning July 2026. Rising catastrophe and inflation costs continued to drive BOP reassessments statewide.

The BOP market in 2025 reflected cautious optimism. Moderate rate increases were balanced with a stronger focus on risk management.

Businesses continue to face ongoing challenges from climate volatility, cyber threats, and litigation trends. Insurers like Liberty Mutual and Hanover demonstrated agility through targeted exclusions and regulatory navigation.

For business owners, preparation remains critical. Risk reviews, early renewals, and partnerships with knowledgeable brokers to secure optimal coverage can support more favorable outcomes. Stay tuned to see how these trends evolve. 2026 promises continued adaptation in this vital sector.

© 2026 Insuraviews. All rights reserved.